Surgical Drains Market Growth, Trends, Share, Demand, Opportunities and Future Outlook 2032

Surgical Drains Market Size- By Type, By Product, By Application, By End User, By End Use- Regional Outlook, Competitive Strategies and Segment Forecasts to 2032

| Published: Dec-2022 | Report ID: MEDE2215 | Pages: 1 - 232 | Formats*: |

| Category : Medical Devices | |||

- March 2020: ConvaTec has added the new ConvaMax Superabsorber wound dressing to their line of advanced wound care products. ConvaMax is used to treat wounds that exude excessively, such as dehisced surgical wounds, leg ulcers, pressure ulcers, and ulcers caused by diabetes in the feet.

- August 2021: The Somavac Svs Smart Suction Technology and surgical drain management platform have been granted a United States patent, according to a statement released by Somavac Medical Solutions, Inc.

| Report Metric | Details |

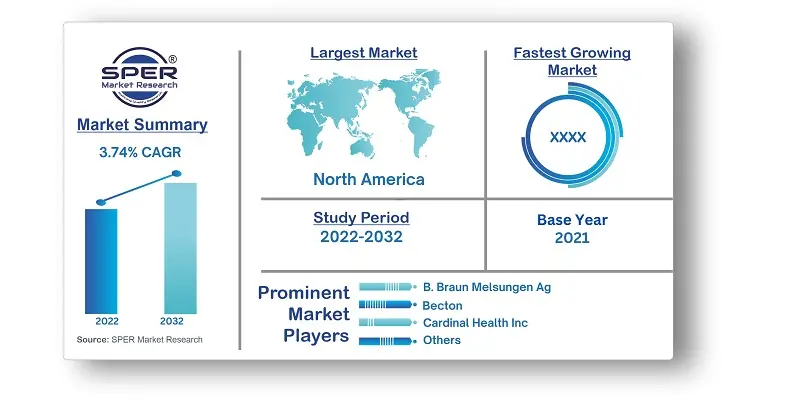

| Market size available for years | 2019-2032 |

| Base year considered | 2021 |

| Forecast period | 2022-2032 |

| Segments covered | By Type, By Product, By Application, By End-User, Bye End-Use |

| Regions covered | North America, Asia-Pacific, Latin America, Middle East & Africa and Europe |

| Companies Covered | B. Braun Melsungen Ag, Becton, Cardinal Health Inc., Convatec Group Plc, Degania Silicone Ltd., Ethicon Us Llc, Johnson & Johnsons, Medline Industries Inc., Romsons Group Private Ltd., Stryker Corporation, Others |

- Surgical drains manufacturers

- Surgical drains suppliers and distributors

- Research and development companies

- Medical research laboratories

- Academic medical centers and universities

- Research and consulting firms

- Venture capital firms

| By Type: |

|

| By Product: |

|

| By Application: |

|

| By End-Users: |

|

- Global Surgical Drains Market Size (FY’2022-FY’2032)

- Overview of Global Surgical Drains Market

- Segmentation of Global Surgical Drains Market By Type (Active Drain, Passive Drain)

- Segmentation of Global Surgical Drains Market By Product (Closed Surgical Drainage System, Open Surgical Drainage System, Surgical Drainage System)

- Segmentation of Global Surgical Drains Market By Application (Cardiac and Thoracic Surgery, Orthopedic Surgery, Obstetric/Gynecological Surgery)

- Segmentation of Global Surgical Drains Market By End-User (Abdominal Surgery, Neurosurgery, Thoracic and Cardiovascular Surgery, Orthopedics)

- Segmentation of Global Surgical Drains Market By End-Use (Ambulatory Surgical Center, Hospitals)

- Statistical Snap of Global Surgical Drains Market

- Expansion Analysis of Global Surgical Drains Market

- Problems and Obstacles in Global Surgical Drains Market

- Competitive Landscape in the Global Surgical Drains Market

- Impact of COVID-19 and Demonetization on Global Surgical Drains Market

- Details on Current Investment in Global Surgical Drains Market

- Competitive Analysis of Global Surgical Drains Market

- Prominent Players in the Global Surgical Drains Market

- SWOT Analysis of Global Surgical Drains Market

- Global Surgical Drains Market Future Outlook and Projections (FY’2022-FY’2032)

- Recommendations from Analyst

1.1. Scope of the report1.2. Market segment analysis

2.1. Research data source2.1.1. Secondary Data2.1.2. Primary Data2.1.3. SPER’s internal database2.1.4. Premium insight from KOL’s2.2. Market size estimation2.2.1. Top-down and Bottom-up approach2.3. Data triangulation

4.1. Driver, Restraint, Opportunity and Challenges analysis4.1.1. Drivers4.1.2. Restraints4.1.3. Opportunities4.1.4. Challenges4.2. COVID-19 Impacts of the Global Surgical Drains Market.

5.1. SWOT Analysis5.1.1. Strengths5.1.2. Weaknesses5.1.3. Opportunities5.1.4. Threats5.2. PESTEL Analysis5.2.1. Political Landscape5.2.2. Economic Landscape5.2.3. Social Landscape5.2.4. Technological Landscape5.2.5. Environmental Landscape5.2.6. Legal Landscape5.3. PORTER’s Five Forces5.3.1. Bargaining power of suppliers5.3.2. Bargaining power of buyers5.3.3. Threat of Substitute5.3.4. Threat of new entrant5.3.5. Competitive rivalry5.4. Heat Map Analysis

6.1. Global Surgical Drains Market Manufacturing Base Distribution, Sales Area, Product Type6.2. Mergers & Acquisitions, Partnerships, Product Launch, and Collaboration in Global Surgical Drains Market

7.1. Global Surgical Drains Market Size, Share and Forecast, By Type, 2019-20257.2. Global Surgical Drains Market Size, Share and Forecast, By Type, 2026-20327.3. Active Drain7.4. Passive Drain

8.1. Global Surgical Drains Market Size, Share and Forecast, By Product, 2019-20258.2. Global Surgical Drains Market Size, Share and Forecast, By Product, 2026-20328.3. Accessories8.4. Closed Surgical Drainage Systems8.5. Open Surgical Drainage Systems8.6. Surgical Drainage Systems

9.1. Global Surgical Drains Market Size, Share and Forecast, By Application, 2019-20259.2. Global Surgical Drains Market Size, Share and Forecast, By Application, 2026-20329.3. General Surgery9.4. Cardiac and Thoracic Surgery9.5. Orthopedic surgery9.6. Obstetric/Gynecological Surgery

10.1. Global Surgical Drains Market Size, Share and Forecast, By End-Users, 2019-202510.2. Global Surgical Drains Market Size, Share and Forecast, By End-Users, 2026-203210.3. Abdominal Surgery10.4. Neurosurgery10.5. Thoracic and Cardiovascular Surgery10.6. Orthopedics

11.1. Global Surgical Drains Market Size and Market Share

12.1. Global Surgical Drains Market Size and Market Share By Region (2019-2025)12.2. Global Surgical Drains Market Size and Market Share By Region (2026-2032)

12.3. Asia-Pacific12.3.1. Australia12.3.2. China12.3.3. India12.3.4. Japan12.3.5. South Korea12.3.6. Rest of Asia-Pacific12.4. Europe12.4.1. France12.4.2. Germany12.4.3. Italy12.4.4. Spain12.4.5. United Kingdom12.4.6. Rest of Europe12.5. Middle East and Africa12.5.1. Kingdom of Saudi Arabia12.5.2. United Arab Emirates12.5.3. Qatar12.5.4. South Africa12.5.5. Egypt12.5.6. Morocco12.5.7. Nigeria12.5.8. Rest of Middle-East and Africa12.6. North America12.6.1. Canada12.6.2. Mexico12.6.3. United States12.7. Latin America12.7.1. Argentina12.7.2. Brazil12.7.3. Rest of Latin America

13.1. B. BRAUN MELSUNGEN AG13.1.1. Company details13.1.2. Financial outlook13.1.3. Product summary13.1.4. Recent developments13.2. BECTON13.2.1. Company details13.2.2. Financial outlook13.2.3. Product summary13.2.4. Recent developments13.3. CARDINAL HEALTH INC.13.3.1. Company details13.3.2. Financial outlook13.3.3. Product summary13.3.4. Recent developments13.4. CONVATEC GROUP PLC13.4.1. Company details13.4.2. Financial outlook13.4.3. Product summary13.4.4. Recent developments13.5. DEGANIA SILICONE LTD.13.5.1. Company details13.5.2. Financial outlook13.5.3. Product summary13.5.4. Recent developments13.6. ETHICON US LLC13.6.1. Company details13.6.2. Financial outlook13.6.3. Product summary13.6.4. Recent developments13.7. JOHNSON & JOHNSONS13.7.1. Company details13.7.2. Financial outlook13.7.3. Product summary13.7.4. Recent developments13.8. MEDLINE INDUSTRIES INC.13.8.1. Company details13.8.2. Financial outlook13.8.3. Product summary13.8.4. Recent developments13.9. ROMSONS GROUP PRIVATE LTD.13.9.1. Company details13.9.2. Financial outlook139.3. Product summary13.9.4. Recent developments13.10. STRYKER CORPORATION13.10.1. Company details13.10.2. Financial outlook13.10.3. Product summary13.10.4. Recent developments13.11. Others

SPER Market Research’s methodology uses great emphasis on primary research to ensure that the market intelligence insights are up to date, reliable and accurate. Primary interviews are done with players involved in each phase of a supply chain to analyze the market forecasting. The secondary research method is used to help you fully understand how the future markets and the spending patterns look likes.

The report is based on in-depth qualitative and quantitative analysis of the Product Market. The quantitative analysis involves the application of various projection and sampling techniques. The qualitative analysis involves primary interviews, surveys, and vendor briefings. The data gathered as a result of these processes are validated through experts opinion. Our research methodology entails an ideal mixture of primary and secondary initiatives.

Frequently Asked Questions About This Report

PLACE AN ORDER

Year End Discount

Sample Report

Pre-Purchase Inquiry

NEED CUSTOMIZATION?

Request CustomizationCALL OR EMAIL US

100% Secure Payment